Computerised accounting systems

Created: August 21, 2013 at 4:18 PM | Updated: May 4, 2023 | By Community Resource Kit

A computerised accounting system is the best option for most organisations as it will allow you to manage your finances accurately and efficiently, and it will also make financial reporting and planning much easier.

There are many computerised accounting packages on the market, so you should be able to find one to suit the needs of your organisation. Choosing the right one is important and your group should do some research before you make the decision. Ask computer experts and sales people, and also check around to see what friends or colleagues in other organisations are using.

Checklist for a computerised accounting system

Features you need to consider are:

- can the system calculate GST and allow you to allocate GST by individual transactions?

- can it track funding or project spending?

- can you produce a full set of financial accounts (profit and loss and balance sheet)?

- are you able to process journal entries (adjustments other than banking)?

- is the system secure and user-friendly? (you can usually get a free trial package before you buy)

Chart of accounts

Once you have chosen your accounting package and installed it, you should set up your chart of accounts. This is a list of all types of income, expenditure, assets, liabilities and equity (see the following sample).

Spend some time considering who will require information from you and what sort of information they will require. This will help you decide how detailed your chart of accounts needs to be. For example, a manager may need to know how much is spent on mobile phones versus landline phones. In that case, you would have two categories for telephone in your chart of accounts, whereas an organisation that does not need that level of information would only have one category for telephone accounts.

Sample chart of accounts

Opening balances

If this is your first financial year, you will have no opening balances to begin with. However, if you are changing to a new accounting system you will need to enter the opening balances from last year's balance sheet (i.e. last financial year's closing balances will become this year's opening balances).

Contacts file

Most accounting systems will require you to set up a contact or card file for each person or organisation you have transactions with. Most systems allow you to add in contact details and notes etc, which you may want to consider if this information is not recorded elsewhere.

Processing transactions

A computerised accounting system may streamline processing and reduce the organisation's work by downloading transactions automatically from a bank feed, ready for you to reconcile. The computerised accounting system may also allow you to generate a bulk payment file that can then be uploaded to your bank account for payment, also a time saving.

Most accounting systems work in the following two ways:

- Processing your transactions direct from the bank statements as money in and money out.

- Entering in invoices to be paid (upcoming payments) and then processing the payment against the outstanding invoice (and vice versa for income).

The first option is quicker as each transaction is only handled once. However, the second option allows you to know how much money is outstanding and how much money is owed to you (creditors and debtors).

You need to consider what is useful for your organisation compared to the extra administration time it takes and the level of accountability and transparency that these processes bring to your financial management.

GST processing

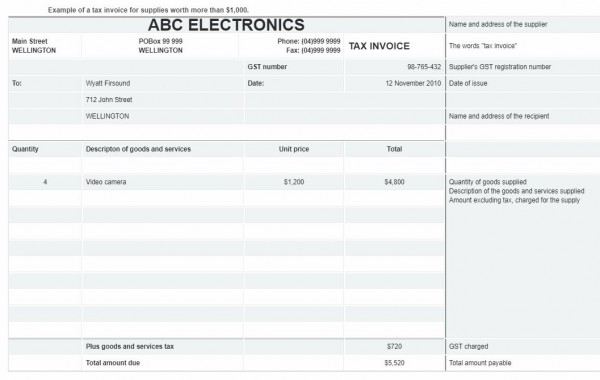

Most accounting systems will ask you to allocate GST (Goods and Services Tax) on each transaction. Some account codes will have a default GST code set up. The code should still be checked before recording. It is also important to check the tax invoice at the time you are entering the information into the system to see if it is a GST tax invoice or not (see sample below).

Sample GST invoice

Example: Tax invoice for supplies worth more than $1000.

Source: Inland Revenue. See also the IRD GST guide (scroll down page) and GST Plus.

Tip: It is important to check the GST status of any grants you receive. Some will have GST added while others will be exempt as they are donations. If you have any doubts, ring your funder to clarify.

Bank reconciliation

It is important to reconcile your bank accounts at least monthly (see the sample below). Most systems will have a separate function to reconcile the banking, in fact many systems allow you to reconcile transactions frequently with regularly updated banking feeds. Once your bank account reconciliation is completed, print off a bank reconciliation report to keep with the bank statements.

Sample monthly bank reconciliation

XYZ Community Group Inc.

Bank Reconciliation for the Month Ended 30 June 2020

To be reconciled (A) must equal (B)

Note: If the bank account and the cash book are in overdraft, the above instructions are changed as follows: ADD becomes DEDUCT and DEDUCT becomes ADD.

Cash book accounting system

While a computerised system makes financial recording, reconciling and reporting easy, a cash book accounting system will work perfectly well for small community groups (particularly groups that are not GST-registered).

A cash book is a spreadsheet, either in a multi-column book or a computer file (see the sample below). It records all financial transactions, keeps you financially up-to-date, and allows you to keep control over your finances.

The cash book keeps track of receipts and payments. It tells you:

- your current bank balance

- how much money has been paid into the bank

- where the money came from

- what cheques have been paid out, to whom and for what

- the total for the month or year for specific purposes e.g. rent

- the total for the month or year for all income and expenses.

Cash book checklist

To operate a cash book:

- use a cash book with as many columns as you think you will need in a manual system, a 16-column book is best

- start each month on a new page (or spreadsheet)

- use the income and receipt columns that are most relevant to your organisation

- where possible, have separate columns for expenses that occur frequently

- make sure you write (or enter) the cheque number or transaction code in the cash book this makes it easier to reconcile with the bank statement

- if you are GST-registered, set up separate columns for GST paid and received (manual cash books are more appropriate for smaller groups that are not GST-registered)

- when you receive your bank statement, enter any automatic payments, bank fees or other items that appear on the bank statement

- add all the columns up at the end of the month and make sure the total of the income columns equals receipts; and the total of the expenditure columns equals payments.

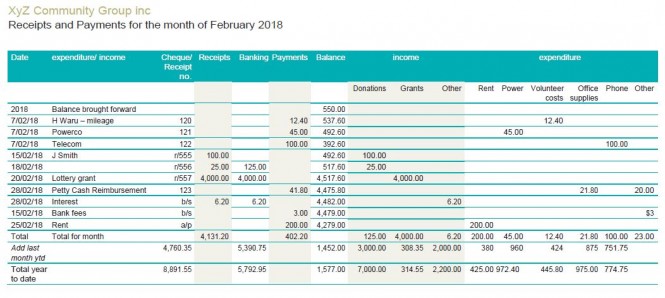

Sample cash book

This example is of a small community group (XYZ Community Group Inc) that is not registered for GST and has no paid staff. The group is using a manual cash book accounting system but the same methods can be applied to a computer spreadsheet.

(This table is also included as a supporting document - you can download it below)

Tip: Balancing the cash book will double-check your figures. The expenditure columns should add up to the payments column and the income columns should add up to the receipts column.

Next page: Financial reporting

Previous page: Financial record keeping

Contents of the Community Resource Kit